The Bank of England’s Base Rate is currently 5.25%; we’re hearing National Savings and Investments offering 6.2% interest rates on deposits, nearly 5% after tax; First Direct offering 7%; these aren’t levels we’ve heard or experienced since 2008!

My question to you is: are these interest rates attracting you away from investing?

Firstly, I think it is worth remembering that the general principles of the economy haven’t changed:

- Governments have to pay higher returns than cash to borrow money.

Governments need to raise money through debt; if cash rates are 5%, Government Bonds have to offer more than that to make it attractive for people to buy them. If you can get a higher interest rate in a fixed rate account with your high street bank, why would you lock your money up for 5 or even 10 years in a Government Bond?

- Companies have to pay more than Governments to borrow.

Similar to the above, companies must make it attractive for you to lend to them rather than the Government. For example, if cash is at 5% and Government Bonds are 6%, Corporate Debt (Corporate Bonds) must be higher, otherwise, why take the additional risk? This all comes back to risk vs reward and our own attitude to risk.

- Equities have to offer the chance of more than, you guessed it, Corporate Bonds.

And again, just further down the chain, companies need to generate a return for their shareholders, as they are taking an increased risk compared to bondholders. Think about it, if shareholders achieve a better return with their money in the banks, soon there would be no shareholders.

What we’re trying to explain here is cash sets the bar, everything else just needs to jump over it.

Of course, it would be lovely to think that this time is different, and today’s investment circumstances are unique: Government debt levels have soared, political turmoil in Ukraine and the Middle East. Include the fast-developing technology of AI…

But is it really?

Between 1993-2007 interest rates averaged at 5.35%, Government debt had risen from 20% of GDP in the 90’s to over 50% in the 00’s, political issues in Middle East and Russia, and the internet was changing society as we knew it.

So, should we have just stayed in cash for all this time? No of course not!

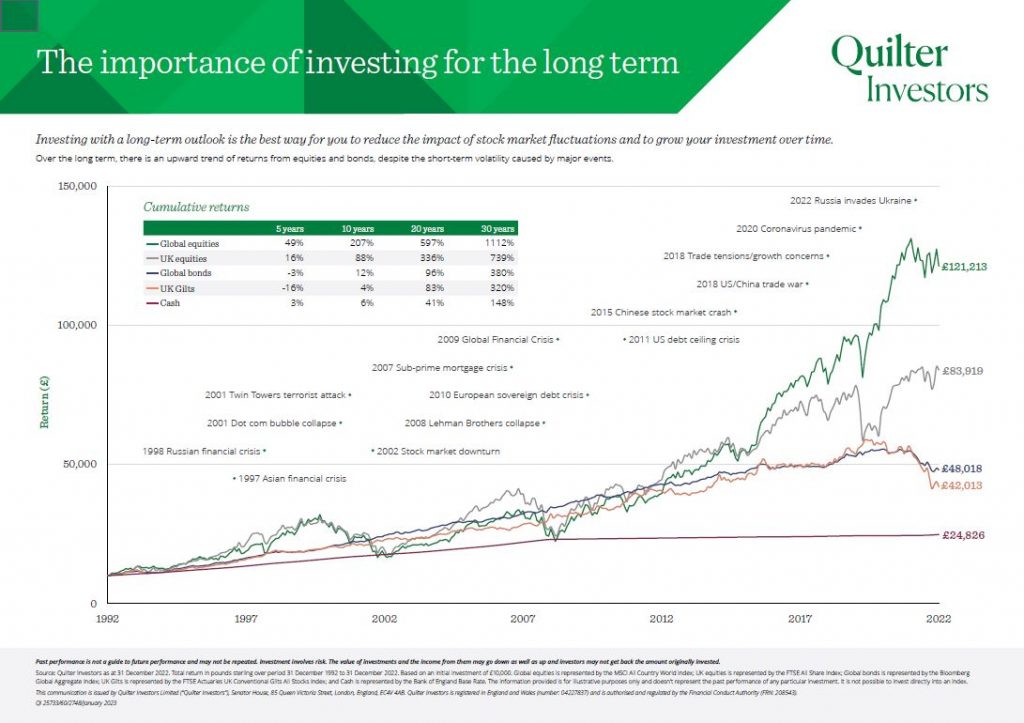

If you’d have invested £10,000 in 1992 and invested as per the Bank of England base rate, at the end of 2022 you would have had £26,325.

Now, if you’d invested that in a multi-asset solution (Bonds and Equities) you would have averaged a return of £89,032.

Which would you rather?

Lucy

Lucy Gilbert – Pension, Investment, Equity Release and Mortgage Adviser at DBFS

Note: Slide included from our friends at Quilter (just for context), but we are fully independent and whole of market, and not promoting Quilter’s products or services.